Contents

- 1 Introduction: Let’s Talk About the Money

- 2 What is funding from the NDIS? (The Big Picture)

- 3 The three main budgets are capital, core, and capacity building.

- 4 Real-Life Example: How One Person Gets Money

- 5 Plan Management: Three Ways to Get Your Money

- 6 Common Beginner Questions About NDIS Funding

- 7 How to Track Your NDIS Funding (Simple Tips)

- 8 Understanding Your NDIS Funding Statement

- 9 Tips for Getting the Most Out of Your Funding

- 10 Conclusion: You’ve Got This

- 11 Ready to Learn More?

Introduction: Let’s Talk About the Money

If you just got your NDIS plan, you might be looking at a piece of paper with a lot of numbers, codes, and categories on it and thinking: What does this all mean? What do I do with this money? And why is it split into so many different parts?

First, take a breath. You are not alone.

The way NDIS funding is structured can feel confusing at first glance. There are terms like “Core Supports”, “Capacity Building”, and “Capital Supports”. There are three different ways to manage your money. And if you get it wrong, you might worry about running out of funds or not being able to pay your support workers.

It’s meant to give you options and control over your supports while making sure the money is spent on things that help you reach your goals.Here is the good news: once you understand the basics, NDIS funding is actually quite logical. It is designed to give you choice and control over your supports while making sure the money is spent on things that help you achieve your goals.

This guide will make it as easy as possible for you to understand NDIS funding. No hard-to-understand words. No legal talk that is hard to understand. Plain English that explains how the money works, how to get to it, and how to make sure you get the most out of your plan.

Let’s get started.

What is funding from the NDIS? (The Big Picture)

Let’s start with the most important question before we get into the details: what is NDIS funding?

The money the Australian government gives you through your NDIS plan is called NDIS funding. NDIS funding, on the other hand, is not like a welfare payment that goes into your bank account and lets you spend it however you want. This means that it can only be used for certain kinds of help that are related to your disability and your goals.

Think of it this way:

Picture getting a gift card for a certain store. You can’t use that coupon to buy gas at the gas station or groceries at the store. You can only use it at that store for certain things. NDIS funding is similar; you have a budget, but it is divided into groups that tell you what you can buy with it.

The goal of this structure is to make sure that the money is used for what it was meant for: helping you live on your own, learn new skills, get involved in your community, and reach your goals.

The three main budgets are capital, core, and capacity building.

There are three different budgets for your NDIS funding. You can’t move money between these three main budgets unless you ask for a formal review of the plan. But you can often move money between sub-categories in one of these budgets, the Core budget.

Let’s look at each one in detail.

1. Core Supports Budget (Your “Everyday” Money)

The Core Supports budget is the part of your plan that can change the most. It includes the things you need help with every day to get through life.

What does Core Supports cover?

- Help with daily tasks like eating, showering, and getting dressed

- Cleaning, laundry, and cooking are all things that need to be done around the house.

- Help with getting around (transport, community involvement)

- Consumables (continence products, cheap tools)

The Four Types of Core Supports:

| Subcategory | What It Talks About | Being flexible |

|---|---|---|

| 01—Help with everyday tasks | Help with personal care, chores, and daily tasks | Core is flexible |

| 02—Help with getting involved in the community and social activities | Support workers can help you get involved in community life, events, and social activities. | Core is flexible |

| 03—Low-Cost Assistive Technology | Simple tools that cost less than $1,500, like shower chairs and walking sticks | Core is flexible |

| 04—Things you need | Everyday things like gloves, continence products, and vitamins | Core is flexible |

The “Flexibility” Rule:

You can move money between these four main subcategories in most NDIS plans. If you need more hours for a support worker but have leftover money for consumables, you can usually use that money to pay for the extra hours. You can’t move Core money into the Capacity Building or Capital budgets, though.

2. Capacity Building Supports Budget (Your “Skills” Money)

The goal of the Capacity Building budget is to help you learn new skills, become more independent, and reach your long-term goals. Most of the time, this money goes to therapists, specialists, and training programmes.

Capacity Building funding is not flexible across categories like Core Supports funding is. You can’t usually move money between categories without first looking over your plan.

The Different Types of Capacity Building:

| Code for the category | Name of the Category | What It Talks About |

|---|---|---|

| 07 | Getting around | The cost of travel if you can’t use public transport because of your disability |

| 08 | Better health and well-being | Physiotherapy, exercise physiology, dietetics, and health support |

| 09 | Better daily life | Occupational therapy, speech pathology, psychology, and behaviour support |

| 10 | Better Relationships | Counselling, training for parents, and services to help with relationships |

| 11 | Better Learning | Programmes for tutoring, skill development, and help with schoolwork |

| 12 | Better Choices in Life | Help with planning, coordinating support, and money matters |

| 13 | Better participation in community and social activities | Programmes that help people connect with their community, learn life skills, and make friends |

| 14 | Better Living Conditions | Help with finding or keeping a place to live, as well as tenancy support |

Most Common Types of Capacity Building for Newbies:

- Category 09 (Improved Daily Living): This is where most therapies, like occupational therapy, speech therapy, and psychology, get their money.

- Category 12 (Better Life Choices): This includes fees for coordinating support and managing plans.

- Category 08 (Better Health and Well-Being): This includes physiotherapy and exercise physiology.

3. Capital Supports Budget (Your “Big Ticket Items”)

The Capital Supports budget is for expensive, long-lasting equipment and changes to your home. These are things you buy once or very rarely that help you stay safe and live on your own.

What does Capital Supports include?

| Type | What It Talks About | For example |

|---|---|---|

| Assistive Technology (Very Expensive) | Tools that cost more than $1,500 and help with moving around, talking, or daily tasks | Hearing aids, hoists, wheelchairs, and communication devices |

| Changes to the Home | Changes to your home to make it safer and easier to get around | Wider doorways, grab rails, ramps and changes to the bathroom |

Important Note: Your plan should usually say how much money Capital Supports will give you. This means that the NDIS has already decided what equipment or changes you need, and the money is only for that purpose. You can’t use the money from Capital Support for anything else.

Real-Life Example: How One Person Gets Money

Let’s use an example to make this real. David is 45 years old and has a spinal cord injury. He uses a wheelchair. He lives by himself and wants to stay that way.

Funding for David’s NDIS Plan:

| Money | Type | Amount of Money | What David Uses It For |

|---|---|---|---|

| Main | Help with Daily Life | Twenty-five thousand dollars | Every day, a support worker comes to help with showering, getting dressed, making meals, and cleaning the house. |

| Main | Things you use up | Three thousand dollars | Gloves, continence products, and supplies for maintaining wheelchairs |

| Main | Community and social | Eight thousand dollars | The support worker takes David to see friends and play basketball every week. |

| Building Capacity | Better Living Every Day (09) | Five thousand dollars | Occupational therapy to check the safety of the home and physiotherapy to keep the upper body strong |

| Building Capacity | Better Choices in Life (12) | $1,500 | Plan manager to take care of all bills and keep track of spending |

| Money | Technology that helps | Eight thousand dollars | A new pressure-relief cushion for his wheelchair (an expensive item) |

How David’s Funding Works in Real Life:

- Every week, David’s support worker sends his plan manager a bill. David’s Core budget pays the bill for the Plan Manager.

- David goes to see his physiotherapist once a month. The physiotherapist sends a bill to the plan manager, who pays it out of the “improved daily living” category.

- David worked with an OT to get quotes when he needed a new wheelchair cushion. The supplier sent a bill to the plan manager, who paid it with money from the capital supports budget.

David never has to worry about turning in claims or keeping track of his balance because he has a plan manager who does it all for him.

Plan Management: Three Ways to Get Your Money

How you manage your money is one of the most important choices you’ll make. This tells you who pays your providers, how you can get your money, and which providers you can use.

You have three choices. Let’s look at them side by side.

Option 1: Managed by NDIA

The National Disability Insurance Agency (NDIA) takes care of your money for you.

- You pick a provider, they send their bill to the NDIA, and the NDIA pays them directly.

- Who you can use: You can only work with NDIS-registered providers.

- Pros: It’s easy. You don’t deal with money. No chance of going over budget.

- Cons: There aren’t many choices for providers. You can’t use unregistered providers, even though they might be more flexible, cheaper, or specialised.

Option 2: Manage Yourself

You manage your own funding. The NDIS pays funds into a dedicated bank account, and you pay your providers directly.

- How it works: You pay providers from your account, then submit claims through the NDIS portal to reimburse yourself.

- Who you can use: You can use any provider—registered or unregistered. You can even hire family members or friends in some circumstances.

- Pros: Maximum flexibility and choice. Often cheaper because you can access non-registered providers.

- Cons: You are responsible for all record-keeping, invoicing, and claiming. It can be time-consuming and stressful if you’re not comfortable with administration.

Option 3: Plan-Managed

You hire a professional plan manager to handle your funding for you.

- How it works: You choose a plan manager. They receive your funding from the NDIA, pay your invoices, track your spending, and handle all the paperwork.

- Who you can use: You can use any provider—registered or unregistered.

- Pros: Best of both worlds. You get the flexibility to choose any provider, but without the administrative burden of self-managing.

- Cons: A small fee is deducted from your plan to pay the Plan Manager (usually around $100–$150 per month, covered by your Capacity Building budget).

Which Option Is Best for Beginners?

If you are new to the NDIS, plan management is often the safest and easiest choice. It gives you the freedom to choose any provider (including smaller, specialised, or more affordable unregistered providers) while taking the stress out of managing money and paperwork.

Common Beginner Questions About NDIS Funding

Let’s answer the questions that most beginners ask when they first receive their funding.

“What happens if I run out of funding?”

If you use up all your funding in a category before your plan ends, you have a few options:

- Check if you can move funds: if you have unused funding in another Core sub-category, you may be able to transfer it to cover the shortfall.

- Request a plan review: If you genuinely need more funding because your circumstances have changed or your plan was inadequate, you can request an early plan review.

- Use your own money: You can always choose to pay for extra support out of your own pocket if you wish.

The best way to avoid running out is to track your spending regularly. A plan manager can help you do this automatically.

“Can I use my funding to pay family members?”

In some cases, yes. If you are self-managed or plan-managed, you can hire family members to provide support—but there are strict rules. The family member must:

- Be genuinely qualified or skilled to provide the support.

- Not be your partner or spouse (generally, you cannot pay a spouse).

- Provide services that are reasonable and necessary.

Always check the NDIS rules or speak to your plan manager before hiring a family member.

“What does ‘stated funding’ mean?”

You may see the term “stated” or “stated funding” in your plan. This means the NDIS has allocated a specific amount of money for a specific support—usually because they believe you need a particular item or service. Stated funding is locked and cannot be used for anything else.

For example, if your plan says “$5,000 stated for wheelchair replacement,” that money can only be used for a wheelchair. You cannot use it for support worker hours.

“Can I change how my plan is managed?”

Yes, you can change your plan management type at any time. You simply need to contact the NDIS and request a change. However, if you switch from NDIA-managed to self-managed or plan-managed, you will need to wait for the change to be processed—which can take a few weeks.

“Do I have to use all my funding?”

No. You are not required to spend every dollar in your plan. However, if you consistently underspend, the NDIS may reduce your funding at your next plan review, assuming you don’t need as much. If you are not using certain supports, it is worth discussing with your planner whether that funding could be redirected to something more useful for you.

How to Track Your NDIS Funding (Simple Tips)

Keeping track of your funding is essential to avoid running out or accidentally overspending. Here are three simple ways to stay on top of it.

1. Use a Plan Manager

If you have plan management in your plan, your plan manager will track your spending for you. Most plan managers provide an online portal or app where you can see your balances in real time.

2. Keep a Simple Spreadsheet

If you are self-managed, create a simple spreadsheet that tracks:

- Date of service

- Provider name

- Amount charged

- Category used

- Remaining balance

Update it weekly to stay on top of your spending.

3. Request a Funding Statement

If you are NDIA-managed, you can call the NDIS and request a current statement of your funding balances. Your Local Area Coordinator (LAC) can also help you check.

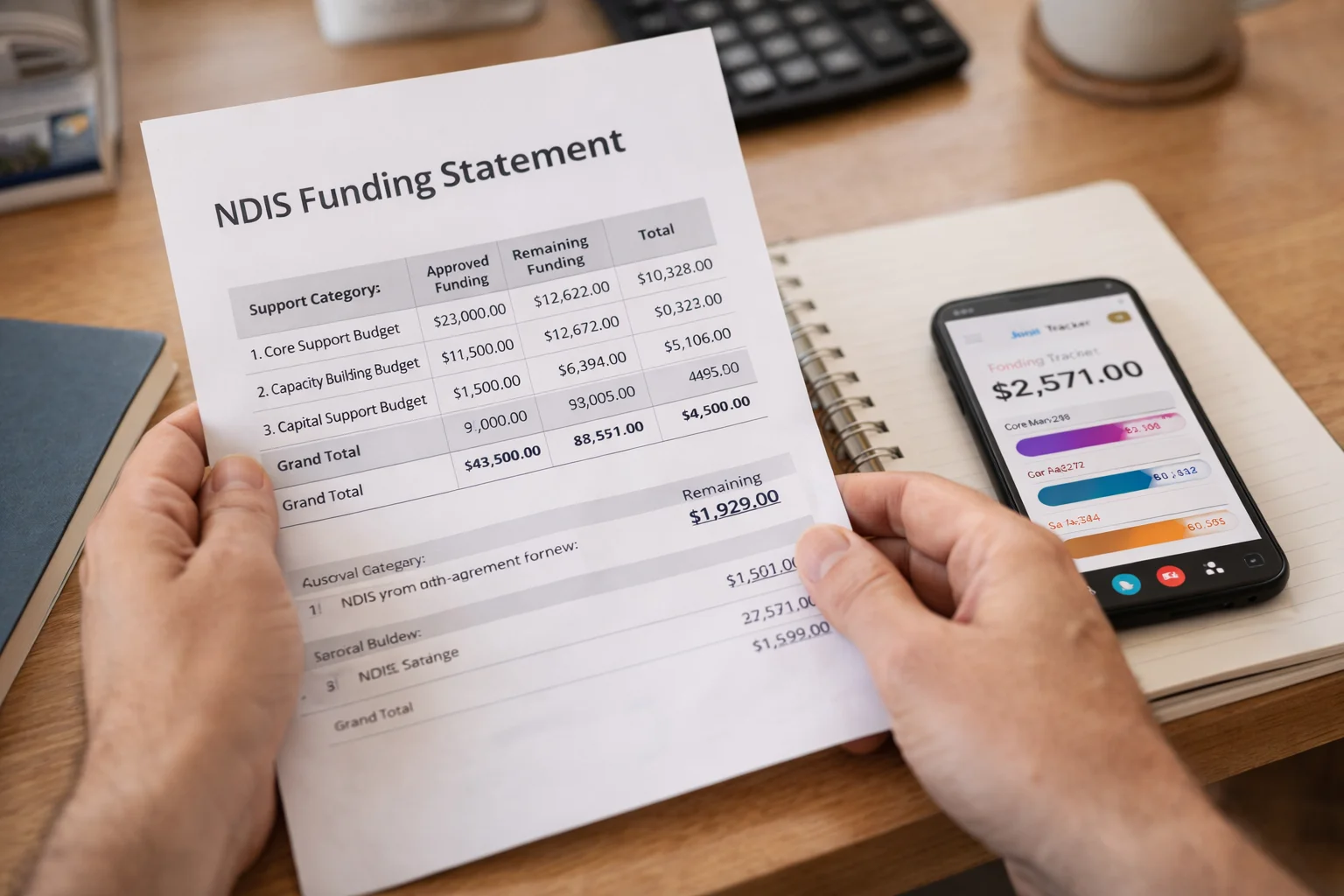

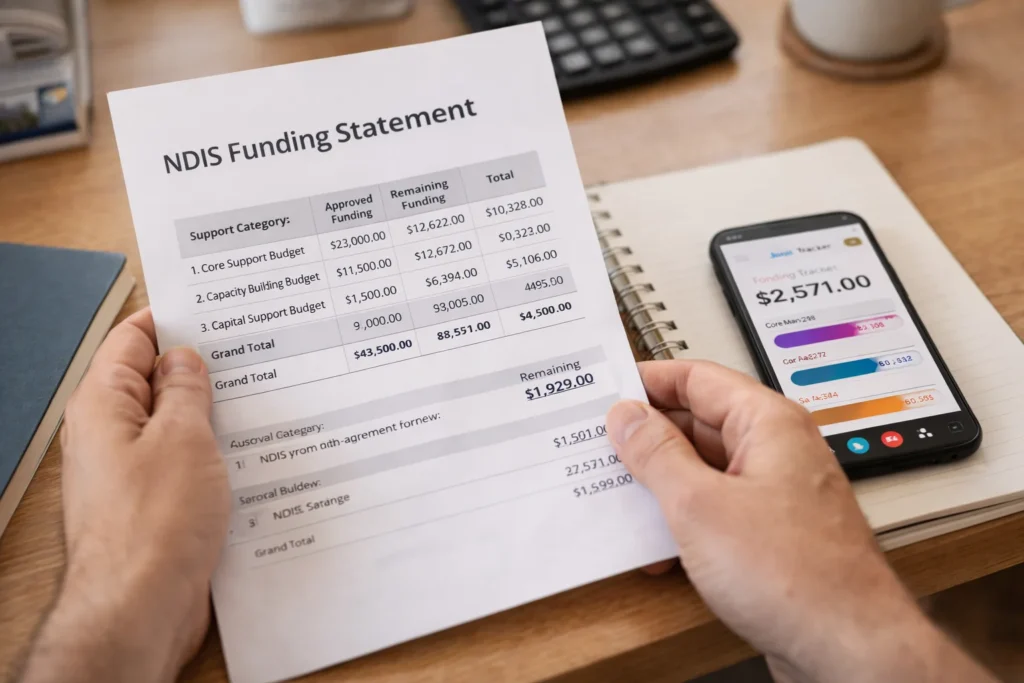

Understanding Your NDIS Funding Statement

When you view your plan in the NDIS portal or through your plan manager, you will see a breakdown of your funding. Here is a simple guide to reading it.

| Term | What It Means |

|---|---|

| Total Allocated | The total amount of funding in that category for your plan period |

| Spent to Date | How much of that funding you have already used |

| Remaining Balance | How much funding you have left to use |

| Plan Start Date | The date your current plan began |

| Plan End Date | The date your current plan ends (usually 12 months later) |

Tips for Getting the Most Out of Your Funding

You’ve worked hard to get your NDIS plan. Now, let’s make sure you use it wisely.

1. Align Spending with Your Goals

Before you spend any funding, ask yourself: Does this support help me work toward my goals? If you are paying for supports that don’t connect to your goals, you may be wasting funding that could be used for something more meaningful.

2. Don’t Be Afraid to Change Providers

If a support worker isn’t a good fit, or a therapist isn’t helping you progress, find someone else. You are in control. Your funding follows you, not the provider.

3. Ask Questions

If you are unsure whether a support is covered, ask. Your plan manager, support coordinator, or LAC can help you understand what is and isn’t allowed.

4. Plan for Your Plan Review

Your plan will be reviewed about 8–10 weeks before it ends. Start thinking early about what worked, what didn’t, and what you want to achieve in your next plan. Keep records of how you used your funding—this evidence will help you advocate for the right funding in your next plan.

Conclusion: You’ve Got This

Understanding NDIS funding can feel overwhelming at first. There are different budgets, categories, and management options. But once you break it down, the system is designed to be logical and flexible.

Let’s recap the key points:

- Your funding is divided into three budgets: Core (everyday supports), Capacity Building (skills and therapies), and Capital (high-cost equipment).

- Core funding is flexible—you can move money between its sub-categories.

- Capacity building and capital funding are usually locked to specific purposes.

- You have three management options: NDIA-managed (simplest, registered providers only), self-managed (most flexible, more admin), and plan-managed (best of both worlds).

- Track your spending to avoid running out of funding.

- You are in control. You choose your providers and how you use your funding to work toward your goals.

The NDIS is a powerful tool to help you live a better life. The more you understand how your funding works, the more confidently you can use it to build independence, connect with your community, and achieve the things that matter to you.

Ready to Learn More?

Understanding NDIS funding is just one step on your journey. Here are some other guides that can help:

- What is NDIS in Australia? A Simple Beginner’s Guide 2026

- Who Is Eligible for NDIS? A Simple Beginner’s Guide for Australians 2026

- How to Apply for NDIS Step by Step: A Beginner’s Guide 2026

- NDIS Plan Explained Simply: 7 Things Every Beginner Should Know

- NDIS Support Categories Explained: 3 Key Budgets Every Beginner Must Understand (2026)

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. NDIS policies and processes may change. Always refer to the official NDIS website or consult with a registered professional for advice specific to your situation.